VA Home Loans: Simplifying the Home Buying Process for Armed Force Employee

VA Home Loans: Simplifying the Home Buying Process for Armed Force Employee

Blog Article

Optimizing the Benefits of Home Loans: A Step-by-Step Strategy to Securing Your Perfect Residential Or Commercial Property

Navigating the facility landscape of home financings needs a methodical strategy to make certain that you protect the residential property that aligns with your economic goals. To absolutely make best use of the benefits of home lendings, one have to consider what steps follow this fundamental work.

Recognizing Mortgage Basics

Understanding the fundamentals of home loans is essential for anyone taking into consideration buying a building. A home mortgage, usually described as a home loan, is a financial item that enables individuals to obtain money to buy realty. The customer consents to repay the funding over a specified term, typically varying from 15 to 30 years, with passion.

Key parts of mortgage include the major amount, rates of interest, and settlement routines. The principal is the amount obtained, while the passion is the expense of loaning that quantity, expressed as a percent. Interest prices can be repaired, continuing to be continuous throughout the car loan term, or variable, fluctuating based upon market problems.

Additionally, debtors need to recognize different sorts of mortgage, such as standard car loans, FHA lendings, and VA finances, each with distinctive eligibility requirements and advantages. Understanding terms such as down repayment, loan-to-value proportion, and private home loan insurance policy (PMI) is also vital for making educated decisions. By grasping these fundamentals, potential home owners can browse the complexities of the home mortgage market and identify choices that straighten with their financial goals and residential or commercial property ambitions.

Assessing Your Financial Situation

Reviewing your financial situation is an essential action before embarking on the home-buying journey. This analysis entails an extensive assessment of your revenue, expenses, cost savings, and existing financial debts. Begin by computing your complete month-to-month revenue, including salaries, bonuses, and any extra sources of profits. Next off, checklist all month-to-month expenditures, ensuring to account for fixed costs like rent, energies, and variable costs such as groceries and home entertainment.

After establishing your revenue and costs, determine your debt-to-income (DTI) proportion, which is vital for lenders. This proportion is determined by dividing your complete monthly financial debt settlements by your gross month-to-month earnings. A DTI proportion below 36% is typically thought about positive, suggesting that you are not over-leveraged.

Additionally, examine your credit rating, as it plays a critical function in securing favorable finance terms. A greater credit rating score can cause reduced rate of interest, eventually conserving you cash over the life of the funding.

/mortgagemarvel/VA_Mortgage_Home_Loans_Florida_Tampa_Clearwater_Macdill_AFB_Wesley_Chapel_Riverview_South_Tampa_Hyde_Park__Unconventional_lending_Derek_Bissen-s7a34.jpg)

Discovering Financing Choices

With a clear picture of your economic circumstance established, the following action includes exploring the different car loan alternatives offered to potential property owners. Comprehending the different kinds of home finances is critical in selecting the best one for your demands.

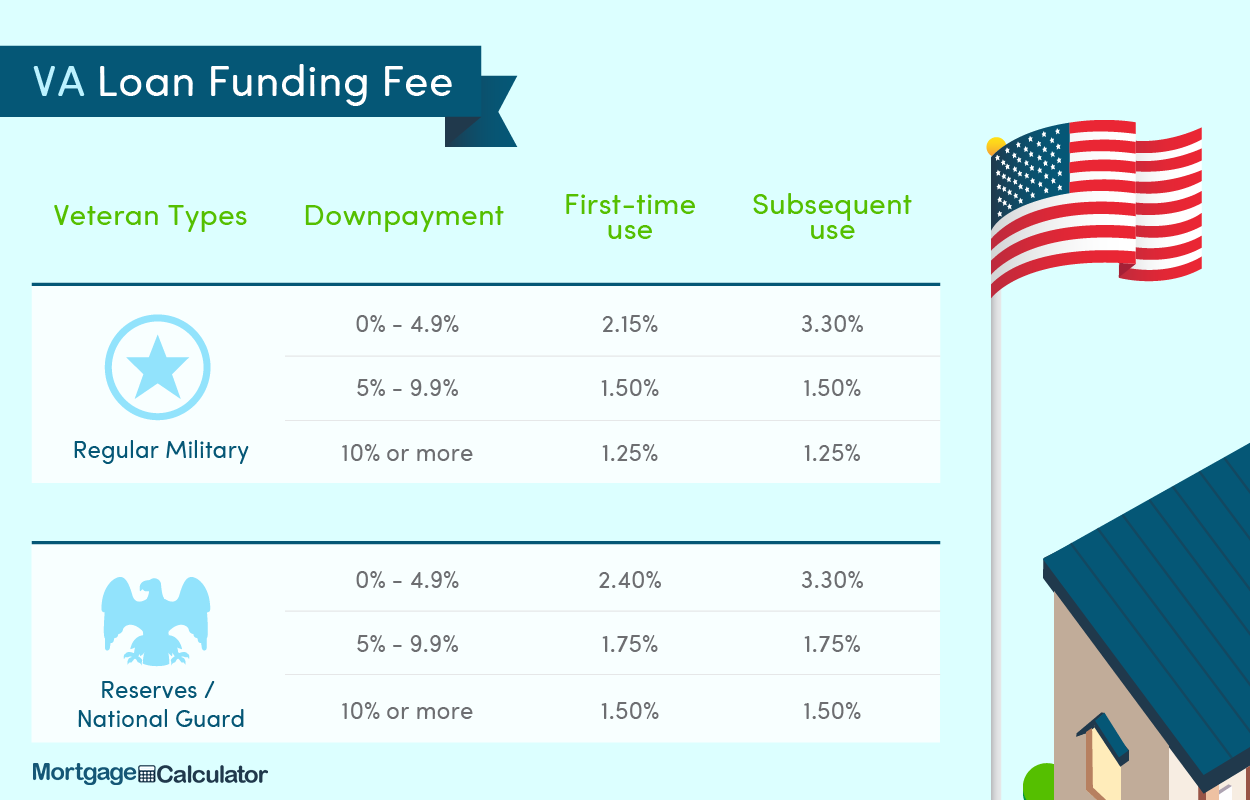

Conventional loans are traditional financing approaches that commonly call for a higher credit history and deposit however offer affordable rate of interest. Alternatively, government-backed finances, such as FHA, VA, and USDA finances, satisfy specific teams and typically require reduced down repayments and credit history, making them accessible for new purchasers or those with limited funds.

One more option is adjustable-rate mortgages (ARMs), which include lower initial rates that adjust after a specified period, potentially causing substantial savings. Fixed-rate home mortgages, on the other hand, provide security with a consistent rate of interest throughout the finance term, securing you against market variations.

Additionally, take into consideration the finance term, which frequently varies from 15 to 30 years. Much shorter terms may have greater monthly repayments yet can save you rate of interest with time. By thoroughly evaluating these choices, you can make an enlightened decision that lines up with your economic goals and homeownership goals.

Planning For the Application

Efficiently preparing for the application process is essential for securing a home funding. A solid credit score is important, as it influences the loan amount and interest prices readily available to you.

Following, gather required documentation. Common requirements include current pay stubs, tax obligation returns, bank statements, and evidence of possessions. Organizing these papers ahead of time can substantially speed up the application process. In addition, take into consideration getting a pre-approval from loan providers. When making a deal on a residential property., this not only gives a clear understanding of your loaning capability however also reinforces your setting.

Additionally, establish your budget by considering not just the financing amount yet also residential or commercial property tax obligations, insurance coverage, and upkeep costs. Ultimately, familiarize on your own with various finance kinds and their particular terms, as this expertise will equip you to make enlightened decisions during the application procedure. By taking these positive actions, you will read the article certainly boost your readiness and increase your possibilities of protecting the home car loan that finest fits your demands.

Closing the Bargain

Throughout the closing meeting, official source you will review and sign numerous records, such as the car loan estimate, shutting disclosure, and home loan agreement. It is vital to completely understand these papers, as they describe the financing terms, payment schedule, and closing expenses. Take the time to ask your lending institution or realty representative any type of concerns you might need to prevent misconceptions.

When all records are signed and funds are moved, you will get the tricks to your new home. Bear in mind, closing expenses can differ, so be gotten ready for expenditures that may include assessment fees, title insurance coverage, and lawyer fees - VA Home Loans. By remaining arranged and informed throughout this process, you can make certain a smooth transition into homeownership, making the most of the advantages of your mortgage

Final Thought

In verdict, taking full advantage of the advantages of home finances necessitates a systematic strategy, encompassing a complete analysis of financial situations, exploration of varied financing options, and meticulous preparation for the application process. By adhering to these steps, possible home owners can boost their chances of securing beneficial financing and accomplishing their property see this website ownership goals. Eventually, cautious navigation of the closing process additionally strengthens an effective transition into homeownership, making certain lasting financial stability and fulfillment.

Browsing the complex landscape of home finances calls for a methodical method to make sure that you secure the residential property that lines up with your monetary goals.Comprehending the principles of home car loans is necessary for anybody thinking about buying a home - VA Home Loans. A home loan, frequently referred to as a home loan, is an economic item that permits people to obtain cash to acquire genuine estate.In addition, debtors need to be mindful of different types of home car loans, such as traditional fundings, FHA financings, and VA financings, each with distinctive qualification requirements and benefits.In verdict, maximizing the advantages of home fundings necessitates an organized method, incorporating a detailed evaluation of economic situations, expedition of diverse financing choices, and thorough preparation for the application procedure

Report this page